Lending to Continuing Care Retirement Communities

by David F. Fomunyam, Supervising Examiner, Federal Reserve Bank of Philadelphia

This article discusses how banks can identify and manage the credit risks associated with lending to a continuing care retirement community (CCRC). Historically, this type of lending was predominantly conducted at large banks. However, a growing number of regional and community banks have recently become involved in providing financing for senior care facilities as the number of facilities increases to meet the demands of an aging U.S. population.1 In addition, bankers are becoming more knowledgeable about providing financial services to investors of CCRCs. Credit extensions to this sector can be profitable and beneficial if the associated risks are identified and managed.

The Aging of America

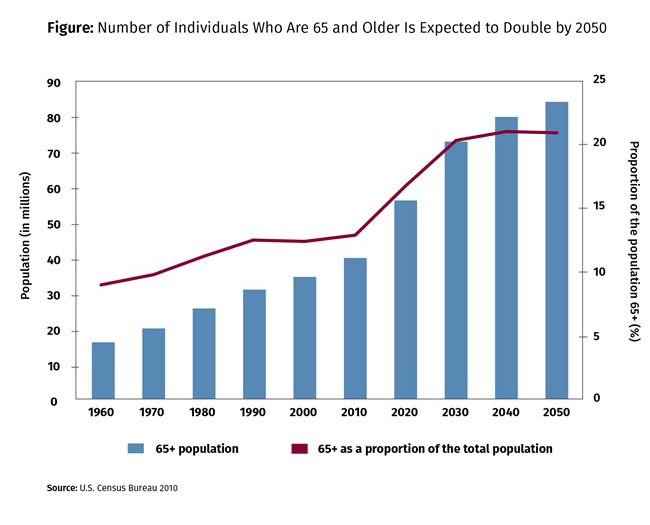

According to 2010 census data, 10,000 people in the United States reach age 65 on a daily basis.2 The data also state that there are 40 million people who are 65 years of age or older. This number is projected to more than double to about 83.7 million by 20503 (Figure). Additionally, the data indicate that seniors aged 85 and older totaled 6 million in 2010; this number is projected to increase to 19 million by 2050.

Factors contributing to longer life expectancy within the overall population include changes in lifestyles such as better diets; cessation of smoking, alcohol, and drug use; and more adherence to wellness and fitness programs. In addition, advances in medicine, including medical technology and medical devices, contribute to prolonged life expectancy and a better quality of life, particularly for the elderly. As the population lives longer, demand in this cohort for specialized housing and long-term care increases. The U.S. Census Bureau publication, 65+ in the United States: 2010, shows that most seniors live in a regular residence. However, the percentage of seniors living in long-term care facilities or community housing with services increases with age.4 For example, only 2.6 percent of Medicare enrollees between the ages of 65 and 74 in 2010 lived in a long-term care facility or community housing with services, but the percentage was 22.2 percent for those over the age of 85.5 As a result, the number of CCRCs in the United States has increased to meet those needs.

The Rise of Continuing Care Retirement Communities

CCRCs date back to the early 1900s, when various faith-based organizations opened retirement communities to care for their elderly members. CCRCs vary in size and configuration, with a typical community consisting of a campus that provides residents a continuum of housing and services choices in one setting. The primary mission of most CCRCs is to provide an environment that enriches the lives and promotes the dignity and self-esteem of their residents. Services provided at a CCRC include necessities of daily living, such as dining, grooming, and social activities, as well as nursing care. Most CCRCs include apartments for independent living, space for assisted living, and beds for skilled nursing care. As the medical needs of seniors increase, CCRCs are adding units for those requiring specialty care for chronic conditions as well as for dementia and other memory-related illnesses. CCRC operations are complex because they provide housing choices, health care, dietary options, hospitality, and recreational activities. In addition, staff must have a wide variety of skills to cover the range of services offered to residents.

The industry experienced rapid expansion during the 1970s and the mid-1980s and attracted some for-profit investors. However, nonprofit organizations continue to dominate this field. According to the National Investment Center, there were 14,000 senior housing and nursing care properties across the country as of the end of 2016.6

A study conducted by gerontology scholar Linda Hollinger-Smith and colleagues on how adult children of current CCRC residents view CCRCs in light of their parents’ experiences “shows that 93 percent of respondents would recommend their family members’ CCRC to others and were likely to consider a CCRC lifestyle for themselves.”7

Types of Loans Used to Finance CCRCs

Because loans secured by a CCRC are in the commercial real estate space, these loans have the same credit requirements as loans secured by other providers of housing services, such as developers and operators of multifamily homes, condominiums, townhomes, cottages, and carriage homes. However, loans to CCRCs are different from traditional housing financing options in several important ways. First, Medicare and Medicaid regulations do not permit assignment of receivables to a lender in the event of a default or bankruptcy. Second, financing a CCRC is complex because actuarial principles for the length of the residents’ occupancy are used for planning and pricing a CCRC’s business model. Third, a disruption in the cash flow assumptions of a CCRC is possible if the CCRC is required to reimburse an individual’s entrance fees (i.e., fees to secure housing in the facility) when the individual leaves the facility.

Credit extensions to a CCRC can include one type of loan or a combination: land acquisition and development loans, construction loans, acquisition loans for an existing facility, refinance loans of existing debt, improvement loans to an existing community, equipment purchase loans, revolving debt loans, and permanent working capital loans. Given the wide choice of loan products, a lender needs to carefully select the loan product that it has the expertise, credit appetite, and capital requirements to support. It is important for underwriters to note that because Medicare/Medicaid receivables cannot be assigned to a lender in a default or bankruptcy, this collateral may not be a secondary source of repayment for a loan.

Evaluating the Financial Condition of a CCRC

The process of evaluating a credit extension to a CCRC is unique. Each CCRC is a standalone operation and should be evaluated on its ability to operate at a profitable and sustainable level.

A CCRC’s financial ratios differ from traditional commercial real estate financial analysis in that the receivables turnover is slower. Most of a CCRC’s receivables are from Medicare and Medicaid, and the government tends to reimburse a CCRC for care and services provided to residents well over 90 days from the billing date. Furthermore, there are strict billing procedures and practices for private insurers as well as for Medicare and Medicaid that must be followed to ensure that the receivable is not rejected or the reimbursement not unduly delayed. An example of an important ratio unique to this industry is the “days cash on hand,”8 which serves as a key measure of a CCRC’s liquidity positions.

Other factors that may impact the cash flow of a CCRC are charitable contributions and investment income, which tend to fluctuate with economic cycles and volatility in the stock market and may also be subject to restricted use. Furthermore, as part of its mission, a CCRC may provide benevolent care9 to residents who qualify for financial assistance or to long-term residents who run out of funds. The level and duration of such care have to be factored in when evaluating the financial condition of the CCRC.

The Commission on Accreditation of Rehabilitation Facilities (CARF)–Continuing Care Accreditation Commission (CCAC) focuses on four major components of a CCRC’s financial results10: margin (profitability) ratios, liquidity ratios, capital structure ratios, and contract type ratios. In analyzing an organization’s financial ratios and trends, it is equally important to benchmark them against other competitors to determine the organization’s strengths and weaknesses.11

Understanding How Market Conditions and Economic Trends Affect CCRCs

The CCRC industry is highly dependent on personal wealth and government assistance. For most retirees, their home is their single largest asset. Most seniors sell their homes to meet the entrance fee requirement for a CCRC contract.12 Because most seniors have to sell their homes before moving into a CCRC, underwriting guidelines should include an analysis of the residential housing market within the footprint where the CCRC is being marketed. Demand for CCRC space is also dependent on general economic conditions. Economic downturns tend to have an adverse effect not only on the residential real estate market but also on the stock and bond markets and consumer sentiment. As a result, demand fluctuations are common in the industry. CCRCs are also subject to the same economic changes that affect the general U.S. economy, such as access to capital, a skilled labor force, and general economic trends and conditions.

Assessing and Managing Risks Associated with CCRCs

Long-term planning and robust risk management practices are critical for the viability of a care provider. The primary assets of a CCRC are its buildings and campus. Because of this, commercial real estate risk is the primary concern when lending to this sector. The customary risks associated with underwriting a commercial real estate loan (for example, appraisal, feasibility studies, demand and supply projections, location, and construction timetable) should be identified and managed in the underwriting process.13 There must be documented and well-supported assessment of the project’s creditworthiness as well as stress-tested scenarios of the borrower’s capacity and ability to perform under difficult circumstances.

Lenders who do not want a long-term asset on their books may opt to finance the construction costs and require repayment from a long-term funding source such as a pension fund, insurance company, or government agency. In such cases, the bank needs to ensure strict adherence to the construction budget and timeline. A permanent lender may require the borrower to achieve occupancy and operating level goals before funding its commitment. An operator’s track record as well as the size and complexity of the project should be diligently assessed for the probability of success.

As is the practice with any prudent commercial loan transaction, the lender should have an understanding of the operator’s business plan and its ability to deliver results that are sufficient to repay debt, meet the expectations of the residents, and comply with regulatory requirements for such facilities. Unlike when loaning to other businesses, it is important for the lender to know and understand the frequency, composition, and complexity of the cash flow stream of a CCRC because of the timing and limits on reimbursement from third parties (for example, private insurance, Medicare, and Medicaid). Entrance fees, which are paid by the resident in exchange for the facility taking the risk of providing future higher-cost services, are another factor that may distort a cash flow stream. These fees are often refundable and are recorded as deferred revenue.

During the underwriting process, the lender should consider the use of covenants, guarantees, reporting requirements, and milestones for financial performance in the loan documents to protect itself and to enable close monitoring of the borrower.

Regulatory and Entrance Barrier Risks

Unlike other commercial real estate projects, a CCRC may have to obtain a certificate of need (CON) from a state to break ground for a new facility. According to the National Conference of State Legislatures, 34 states currently maintain some form of CON requirement for skilled nursing facilities. The basic assumption underlying the regulation is that oversupply of health-care facilities results in health-care price inflation. Price inflation occurs when an operator cannot fill all its beds and fixed costs have to be met by charging more for beds in use. Like any other construction project, a CCRC developer should have the appropriate zoning, building, easement, and utility permits and variances. It is a prudent practice to include these intangible items in the loan documents and assign them to the bank in the event of default.

The operators of CCRCs must also comply with local, state, and federal regulations governing the level and quality of care provided to residents as well as regulations pertaining to standards and condition of the facilities. Noncompliance and repeat violations can lead to suspension of payments or revocation of an operator’s license. In this regard, a lender should request and review all inspection records that relate to quality of care, building code violations, and other reports incidental to operating the facility and as well all corrective actions taken to remediate concerns or violations.

Actuary Risk

CCRC finances are complex because actuarial principles are used for planning and pricing models. The actuarial model assumptions have to be reasonable to ensure that the operator can appropriately price the future cost for assisted and skilled care. The residents pay a graduated entrance fee based on the level of future care desired. These fees are used to cover future benefits promised to the residents when they sign an agreement to enter a CCRC. These actuarial assumptions are becoming increasingly difficult to project in light of improvement in life expectancy for all age groups and gender.

Reimbursement Risk

Reimbursement risk can occur if a payment to a CCRC in return for services rendered to a resident of the facility is delayed or not received at all. Private pay residents and private insurance companies usually promptly pay the full amount billed for services provided by the CCRC. However, for Medicare and Medicaid residents, the reimbursement amounts are significantly less — about 70 percent of the cost to care for a beneficiary. Reimbursement risk has to be well managed by a CCRC by ensuring that the number of private pay and private insurance residents far exceed Medicare and Medicaid beneficiaries.

Conclusion

People are living longer, and they want the ability to live independently but still have the convenience of, for example, seeing a medical professional in the same facility. Therefore, CCRCs have become a highly desirable option to the aging population. Underwriting credit extensions to a CCRC is challenging. It differs from traditional commercial underwriting because it combines risk elements from various external factors. Credit extensions to investors in CCRCs can be profitable and beneficial if the associated risks are identified and managed. Commercial real estate risk is the primary concern when lending to this sector because the primary assets of a CCRC are its buildings and campus. The lender needs to have an understanding of the CCRC’s business plan and ability to consistently execute that business plan and deliver superior results sufficient to repay debt, meet the expectations of the residents, and comply with regulatory requirements.

Back to top- 1 John Reosti, “Growth of Senior-Care Facilities Presents Opportunity for Lenders,” American Banker, August 12, 2016, available at www.americanbanker.com/news/growth-of-senior-care-facilities-presents-opportunity-for-lenders.

- 2 See 2010 census data, available at www.census.gov/programs-surveys/decennial-census/data/datasets.2010.html.

- 3 Jennifer M. Ortman, Victoria A. Velkoff, and Howard Hogan, An Aging Nation: The Older Population in the United States, U.S. Census Bureau, Report Number P25-1140, May 2014, available at www.census.gov/library/publications/2014/demo/p25-1140.html.

- 4 As defined in the report, “long-term care facilities” are certified by Medicare or Medicaid, while “community housing with services” are residences that include a retirement community, a continuing care retirement facility, an assisted living facility, or a similar situation. See Loraine A. West, Samantha Cole, Daniel Goodkind, and Wan He, 65+ in the United States: 2010: Current Population Reports, June 2014; available at www.census.gov/content/dam/Census/library/publications/2014/demo/p23-212.pdf.

- 5 See 2014 census data available at www.census.gov/

content/dam/Census/library/publications/2014/demo/p23-212.pdf. - 6 The National Investment Center is a leading provider of timely and comprehensive performance data on the senior housing and care industry.

- 7 Linda Hollinger-Smith, Kathryn Brod, Susan Brecht, and Mary Leary, “Adult Children of CCRC Residents: Their Perceptions, Insights, and Implications for Shaping the Future CCRC,” Seniors Housing & Care Journal, 20:1 (2010), pp. 3–20.

- 8 This ratio is used to determine the number of days the borrower can pay his or her operating expenses from available cash.

- 9 Benevolent care programs enable residents to remain at the facility after they have exhausted their financial resources.

- 10 The CARF–CCAC Financial Advisory Panel is a for-profit advisory group that provides financial ratios and trends for the Continuing Care Retirement Community. This publication provides key data for evaluating the financial condition of a CCRC as well as peer ratios for comparison.

- 11 Kevin Mulhearn, Financial Ratios and Trends of CARF–CCAC Accredited Organizations, 2009, Tuscon, AZ: Commission on Accreditation of Rehabilitation Facilities.

- 12 Robert Andrews, “Assisted Living Communities: How a Changing Population, Health Care Reform, and Changes in State Regulations Will Continue to Drive Growth,” RMA Journal, September 2010, available at cms.rmau.org/uploadedFiles/Credit_Risk/Library/RMA_Journal/Economic_Environment/Assisted%20Living%20Communities.pdf.

- 13 See the FedLinks Bulletin “Sound Risk Management of CRE Credit Concentrations” from December 2018, available at https://communitybankingconnections.org/assets/fedlinks/2018/20181217-dec-fedlinks.pdf.