Success with Succession Planning Q&A

by Romel Bonilla, Supervision Manager, Supervision and Regulation, Federal Reserve Bank of Chicago, Joel D’Souza, Senior Examiner, Supervision and Regulation, Federal Reserve Bank of Chicago, and William Mark, Lead Examiner, Supervision and Regulation, Federal Reserve Bank of Chicago

This article is a follow-up to “Putting the Success in Succession Planning and Management,” which appeared in the Second Issue 2021 of Community Banking Connections,1 and the July 27, 2021, Ask the Fed2 webinar on succession planning. Both the article and the webinar stressed the importance of succession planning, highlighting this endeavor as a key governance and risk management tool. This follow-up article answers several questions submitted by Ask the Fed audience members during the presentation.

On the Horizon

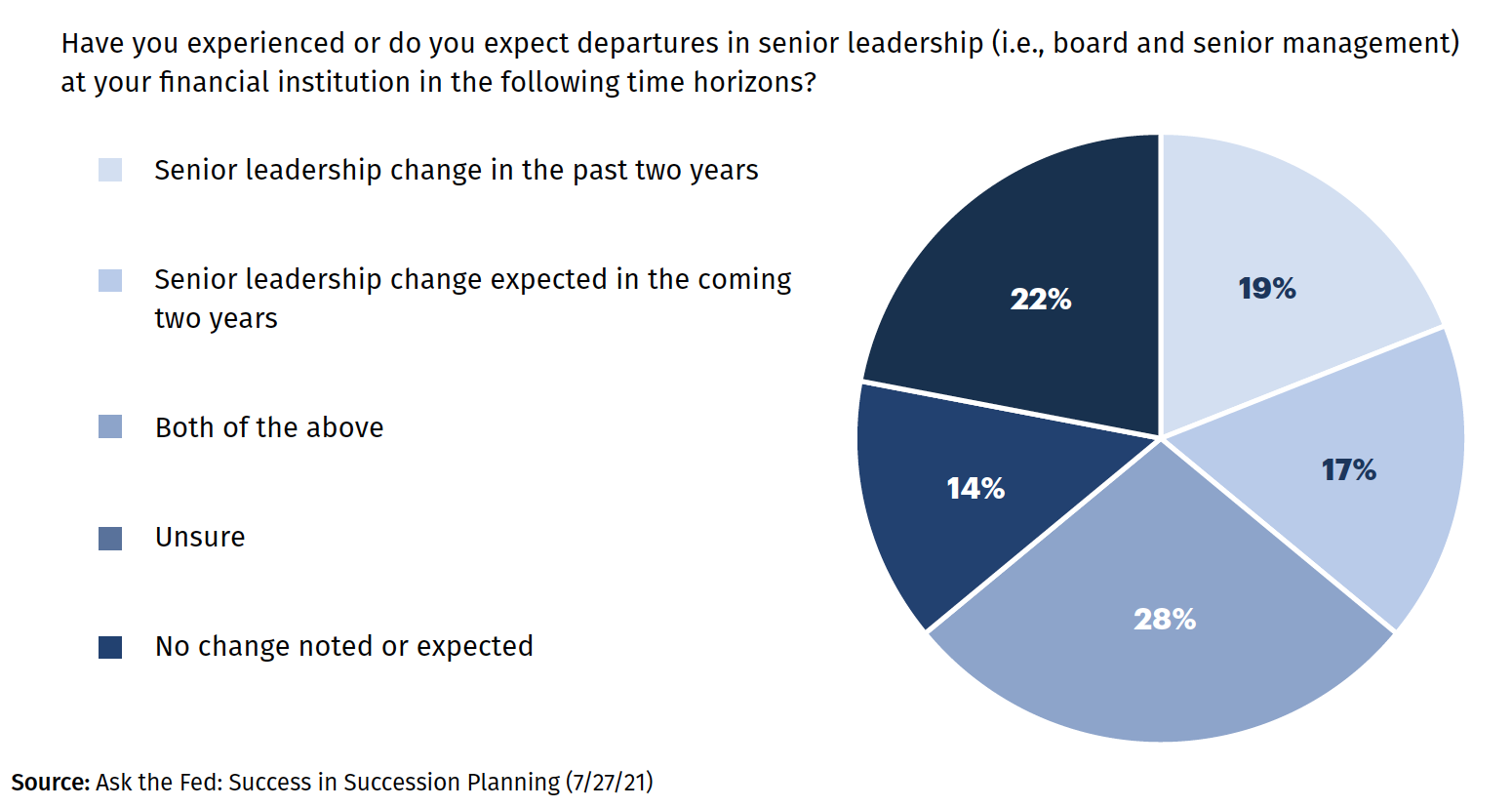

Staff and management turnover are an inevitable occurrence; therefore, a bank should assess its talent resources and plan accordingly. Determining a bank’s talent needs is a challenge that requires short- and long-term perspectives. As indicated in Figure 1, the audience’s responses to the Ask the Fed’s polling questions reinforced the importance of effective succession planning. Sixty-four percent of the participants reported that a change in senior leadership had occurred in the prior two years, that a change is expected in the coming two years, or both.

Figure 1: Turnover in Senior Leadership

Supervisory Perspective

When assigning a bank’s supervisory rating, do examiners consider the composition of the bank’s board of directors, the skill and subject matter expertise of the bank leaders (i.e., information security, business continuity planning, and compliance), or all the above?

In assessing the adequacy of a bank’s management, Federal Reserve examiners assess the ability of its board of directors and management to ensure that the bank is operating in a safe and sound manner, considering the size and complexity of the bank’s operations. Therefore, bank leadership is expected to exhibit relevant experience, display sustained competence, and demonstrate a high level of integrity.

Discuss how much attention is paid to succession planning during a routine examination. Is it part of the pre-examination risk assessment that may be excluded based on risk, or is it something that examiners review at each examination?

Management capabilities and succession prospects are considered throughout the examination process, influencing pre-examination planning strategies and factoring into the assessment of the bank’s viability. Management depth and succession are important considerations for the management rating.3

Supervision and Regulation (SR) letter 16-11, “Supervisory Guidance for Assessing Risk Management at Supervised Institutions with Total Consolidated Assets Less Than $100 Billion,”4 discusses the role and responsibilities of a bank’s board of directors and senior management in overseeing risk management. This letter notes that “the board of directors should collectively have a balance of skills, knowledge, and experience to clearly understand the activities and risks to which the institution is exposed, and senior management should ensure that the activities are managed and staffed by personnel with the knowledge, experience, and expertise consistent with the nature and scope of an institution’s activities and risks.” In assessing the adequacy of risk management, examiners would weigh these factors relative to strategic focus and direction as well as the succession planning process.

For small community banks, would an informal succession plan be sufficient? Or should a formal plan be required regardless of the bank’s asset size?

Whether a succession plan is formal (i.e., written) or informal (i.e., not written but discussed among the board and senior management) will depend on the asset size and complexity of the organization. Strategic and logistical variables will vary from bank to bank and will influence a bank’s planning process. A less formal succession plan could be appropriate for the needs of a small, noncomplex community bank. However, leadership should be mindful that succession plans address the implementation time frame, which will vary depending on the nature of a management change. Further, a sudden and unexpected departure of a bank’s management team member will likely be an “in an emergency, break glass” moment and, therefore, communication and transparency on leadership changes should also be factored into determining the level of formality in succession plans.

How should a bank document its succession plan?

There are no specific regulatory requirements for how a bank should document its succession plan. That said, a bank should consider the level of detail in a plan such that the board of directors and senior management are aware of the action that will need to be taken when there are leadership and staff departures. Such transparency would serve to guide management and staff through the various aspects of the organization’s process to identify, develop, assess, and transition leadership candidates. From a governance perspective, evidence that succession planning is addressed by a board of directors would be considered a safe-and-sound practice.

Challenges and Obstacles

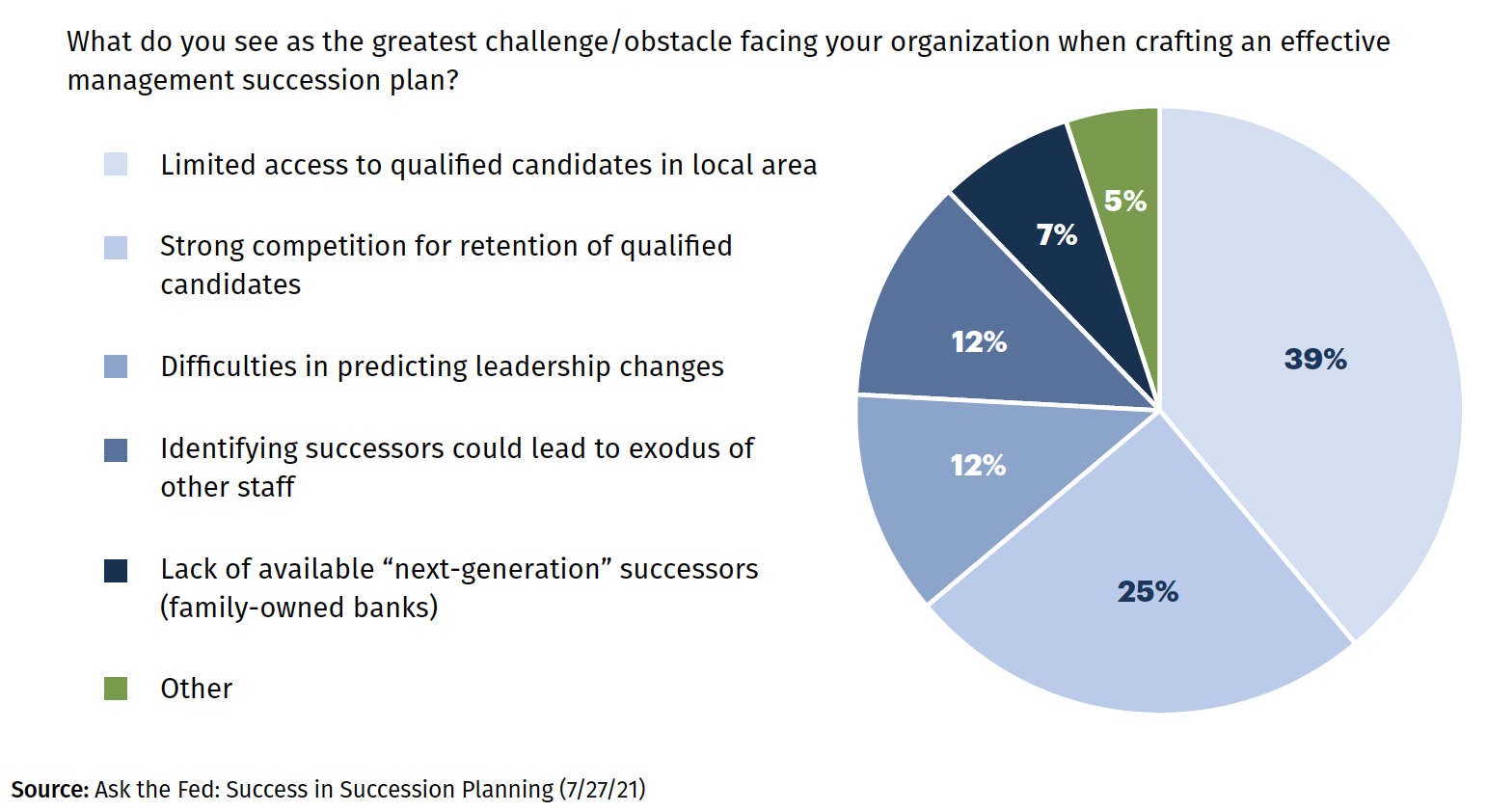

A community bank may face various challenges to developing and maintaining an effective succession program. These potential hurdles include availability of qualified candidates, offering competitive salaries, and retaining the bank’s cultural characteristics. In addition, a bank’s day-to-day business activities may push succession planning, rightly or wrongly, to a lower priority.

Figure 2 illustrates these challenges. Sixty-four percent of the Ask the Fed participants acknowledged that access to qualified candidates can be difficult (i.e., limited access and strong competition). Shifting workforce and demographics in the community the bank serves, strong competition, and budget constraints were cited as hindering the ability to attract and retain qualified individuals.

Figure 2: Challenges and Obstacles

What is the optimal lead time to prepare (or update) a succession plan? Too early is risky, too late is risky. Is there a Goldilocks time frame?

The timing of leadership changes can be difficult to predict, which presents challenges in establishing a planning time horizon as well as a time frame for identifying and developing future leaders. Management transition ambiguities can also stymie or even immobilize a planning process. Additionally, there can be confidentiality concerns, from legal and morale perspectives. If a successor is even identified, the first and second “runners-up” could choose to leave the bank or become dissatisfied with their career opportunities. Therefore, a plan should consider when to disclose the management succession plan to staff.

There is also the downside risk of choosing a successor who turns out to not have the skills, knowledge, or even cultural fit to assume a more demanding leadership role. The specter of this possibility could lead to a sort of “paralysis by analysis” that could delay decisions on identifying a successor candidate. Therefore, the board of directors should position management and staff to facilitate smooth transitions to minimize disruptions to bank operations. With this mindset, a bank could include career development planning and discussion as part of its employee performance process.

How often should succession planning take place in a small, family-owned bank?

Small, family-owned community banks face unique challenges in naming a successor, as there may be limited management and staff resources. These banks often restrict senior management to family members and, therefore, may face a lack of interest or a qualified pool from family members who want to or can fill critical management positions. Nevertheless, while succession planning may be difficult, it would be prudent for the bank’s board of directors to revisit its succession plan on a periodic basis and consider when current leaders may wish to reduce their day-to-day management responsibilities.

How do you overcome statutory limitations (i.e., statutory requirements for the job posting and interview process) that could impede a bank’s ability to plan management succession?

Certain state employment laws cover the timing and procedural requirements for the selection of a successor, which could extend the management selection and transition time frame. These laws are intended to ensure that companies engage in a thoughtful candidate consideration process. Therefore, the timeline for identifying and selecting a candidate to fill key management positions should be considered in the succession planning process to avoid disruption in bank operations. One option is for the plan to designate interim managers for key positions as the selection process is underway.

Responsibilities and Methods

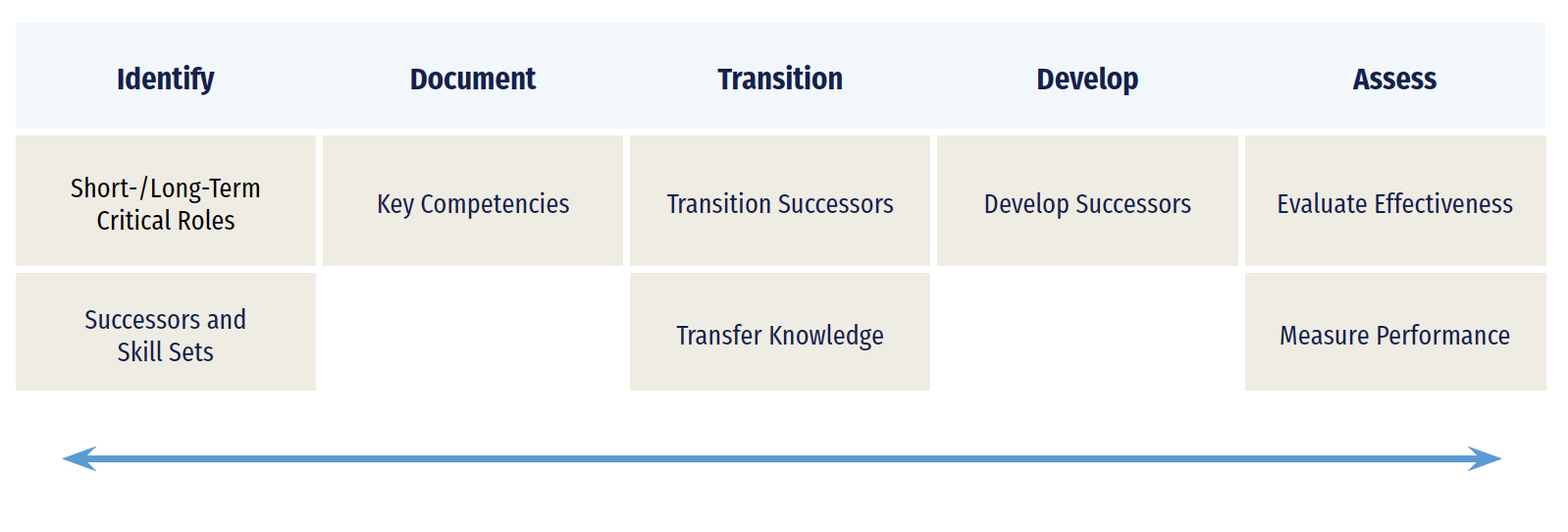

What are some of the key characteristics that examiners see in banks’ succession plans?

Examiners have noted that effective succession plans typically consider critical roles, key competencies, transition exposures, and a strategy for developing and evaluating management candidates as highlighted in Figure 3. Conceptually, this can take the form of a bank identifying key positions and potential successors through a cascading tier structure or distribution of key executive position responsibilities among several individuals. When appropriately structured, this planning exercise can contribute to accomplishing both short- and long-term succession goals. However, it is important that senior leadership tailor its succession plan to the unique nature of its organization. A flawed or incomplete succession plan could expose the bank to excessive transition risk when there is a sudden or unexpected departure of a senior leader or key employee.

Figure 3: Succession Planning Process

Source: Romel Bonilla, Joel D’Souza, and William Mark, “Putting the Success in Succession Planning and Management,” Second Issue 2021 Community Banking Connections, pp. 11–16, available at www.cbcfrs.org/articles/2021/i2/succession-planning-management

Is backup staffing sufficient for senior management succession? To what extent should cross-training of management replacements be expected?

In certain situations, backup staff may be positioned to replace senior management for short-term absences to fulfill day-to-day duties. However, this may not be sufficient for succession planning, as backup staffing alone does not necessarily translate to a long-term strategy. When a backup staff member has been identified as a potential successor, succession planning would create an opportunity for the bank’s senior leadership to evaluate the individual’s performance and share constructive feedback for future career development.

Cross-training can be used to address planned and unexpected staffing changes. Operational disruptions arising from the loss of any individual are partially mitigated when the bank has sufficient “bench strength” — employees who are prepared to assume management responsibilities, if only on an interim basis. A bank can diversify employee skills through cross-training and other development methods such as having an employee serve on a committee or special project or attend an industry conference. Through cross-training, an individual has opportunities to establish coaching and mentoring relationships. Together these opportunities allow potential successors to develop and expand their knowledge about the bank’s operations and management.

Should a bank use a profit-sharing program to retain its top talent?

Compensation arrangements are important tools that a bank can use to attract and retain skilled staff. The board of directors should ensure that its incentive compensation arrangements properly align the interests of both the bank and its employees. Because community banks typically face competition for skilled, experienced staff who are interested in the community banking industry, training programs and compensation strategies (i.e., profit-sharing initiatives) can be used to attract and retain individuals capable of fulfilling leadership roles.

The Diversity Paradigm

Were any top-performing, diverse banks in rural, less-diverse areas?

While there have not been studies that specifically targeted smaller banks operating in rural, less-diverse areas, it is widely acknowledged that teams with diverse experiences can slow the progression to groupthink, the phenomenon in which leaders with similar backgrounds tend to align in thought and gravitate toward the same strategies. Therefore, regardless of a bank’s size, complexity, or location, discussion of alternative viewpoints can contribute to a diversity of thought strategy and advance success at the bank.

Observed Industry Practices

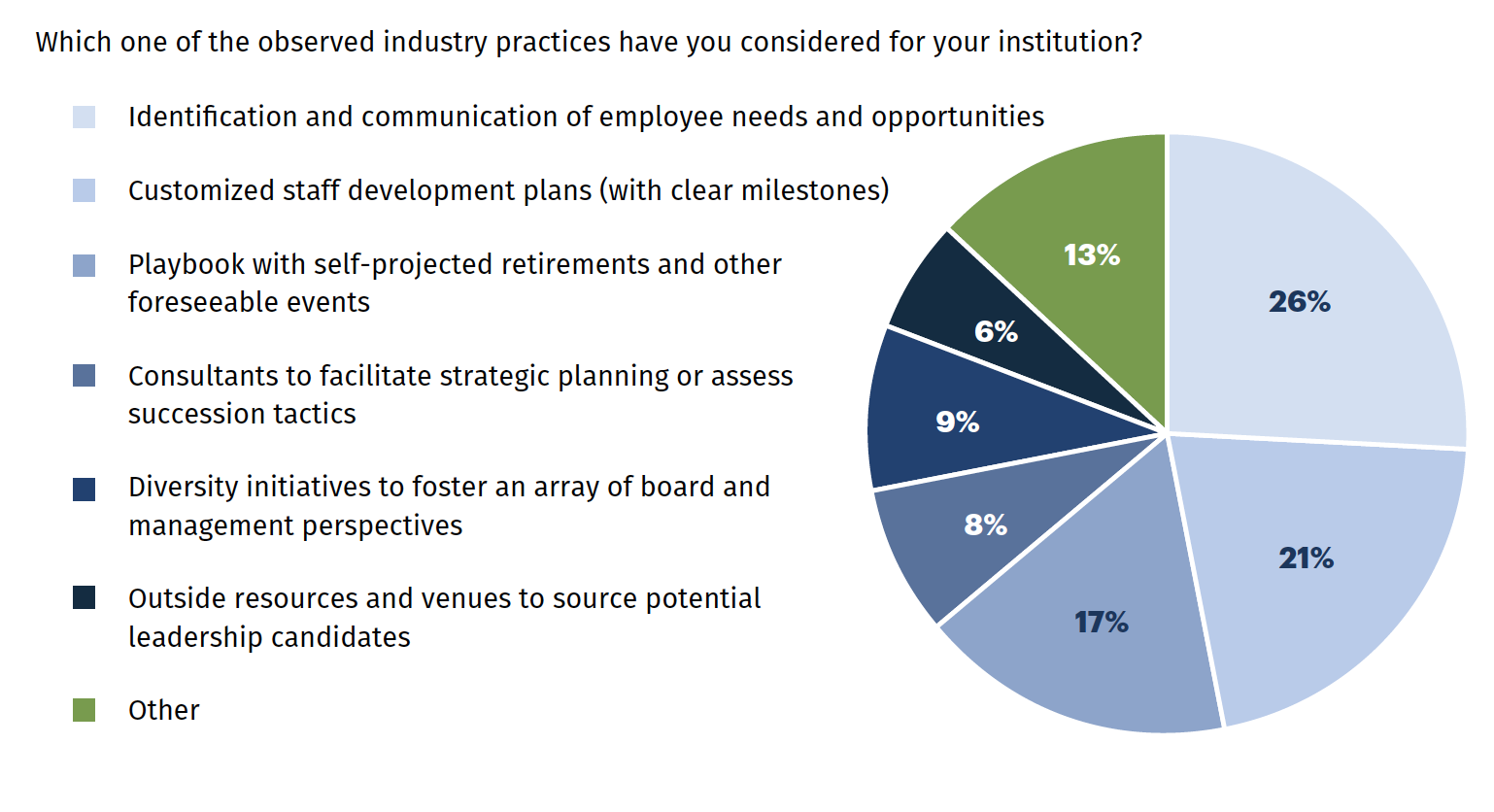

The final question posed to the Ask the Fed audience was about industry practices relative to succession management techniques (Figure 4). Forty-seven percent of the respondents noted that they considered a staff-focused approach to succession planning by identifying and developing employees as the most appropriate practice. Further, 17 percent of the respondents indicated that they use a playbook with self-projected retirements and position readiness indicators for senior management and the directorate. Diversity initiatives to foster a wide array of viewpoints from leadership were considered by 9 percent of the respondents, and 8 percent turned to consultants to supplement planning tactics.

Figure 4: Preferred Industry Practices

Source: Ask the Fed: Success in Succession Planning (7/27/21)

Final Thoughts

Succession planning is essentially a risk management tool designed to minimize the adverse effects of transition risk related to leadership change. Given the importance of maintaining qualified bank leadership, any significant disruption in the bank’s operations can have far-reaching, negative ramifications for a bank’s safety and soundness. Hence, an effective successor management plan is nimble enough to respond to changes in bank leadership in a timely fashion. Therefore, the succession plan should address a bank’s management resources and skill sets, while considering economic conditions and strategic business plans to support the viability of the bank.

- 1 The article is available at www.cbcfrs.org/articles/2021/i2/succession-planning-management.

- 2 The webinar is available on the Ask the Fed website; see https://bsr.stlouisfed.org/askthefed/Home/DisplayCall/310.

- 3 See SR letter 96-38, “Uniform Financial Institutions Rating System,” available at www.federalreserve.gov/boarddocs/srletters/1996/sr9638.htm.

- 4 See SR letter 16-11, “Supervisory Guidance for Assessing Risk Management at Supervised Institutions with Total Consolidated Assets Less Than $100 Billion,” available at www.federalreserve.gov/supervisionreg/srletters/SR1611a1.pdf.